Is Gold Broken? Consolidation Despite Geopolitical Escalation

Commodity Report #243

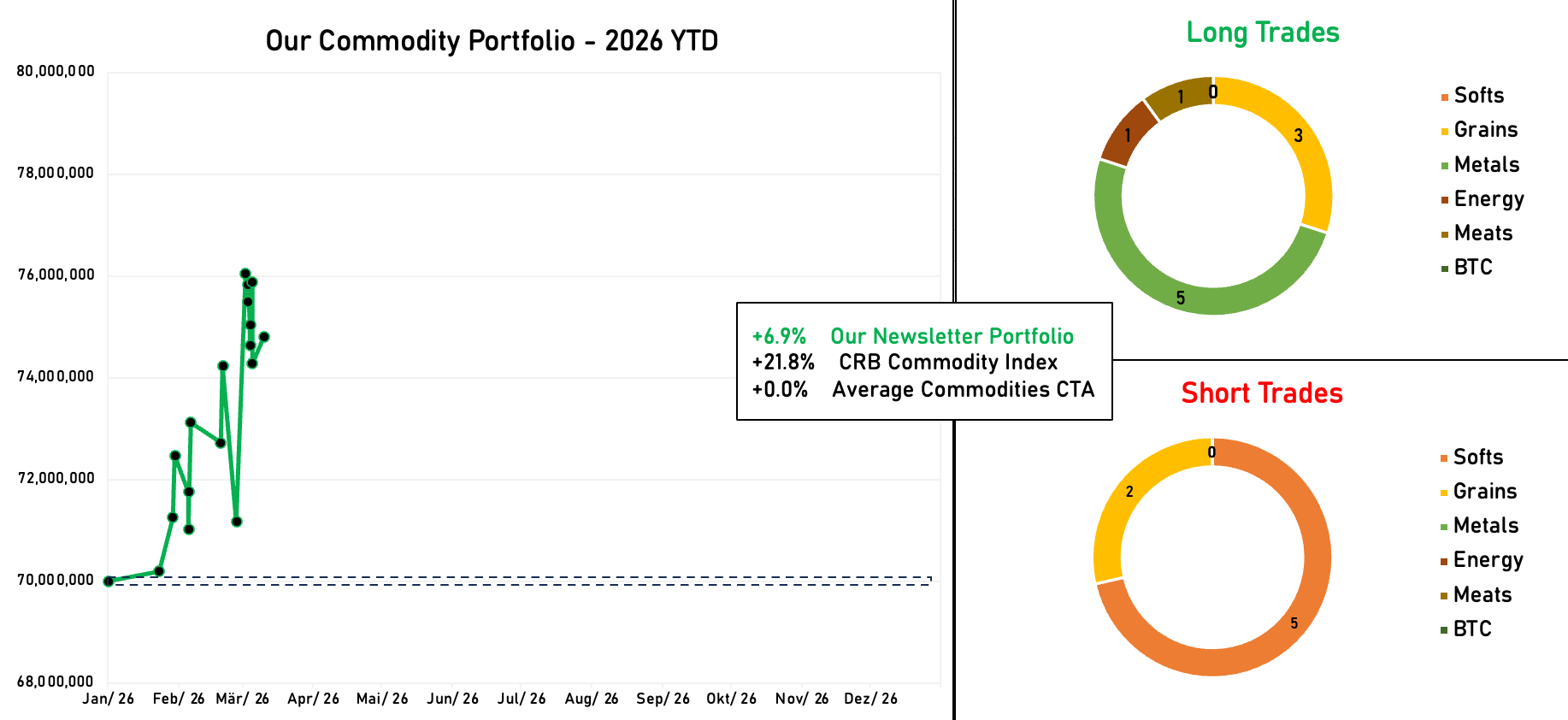

*YTD our absolute return strategy is up +6.9%

Find our 2025 performance here (+20% total return and 2.99 Sharpe)

Is Gold Broken? Consolidation Despite Geopolitical Escalation

Gold has been consolidating over the past two weeks - even though the escalating Iran conflict would typically be expected to drive prices higher. The metal’s muted reaction has left many market participants puzzled.

UBS explains why this is historically less surprising than it may seem: Gold’s track record as a safe haven during military conflicts is mixed - something the current price action reflects. For those seeking a direct hedge against the Middle East conflict, oil remains the better instrument. Gold offers less protection against the conflict itself, but rather against its monetary and financial side effects - think inflationary pressure, currency devaluation, or fiscal dislocations.

Private Credit…

Also noteworthy - the private credit complex. It remains under market stress.

A liquidity crisis in private credit may temporarily push gold prices down, even though gold is a safe-haven asset. If private credit funds impose withdrawal gates during market stress, investors who need cash cannot sell those illiquid positions. Instead, they must liquidate the most liquid assets on their balance sheets, such as gold.

Similar dynamics occurred during the 2008 Financial Crisis and the COVID-19 Market Crash of March 2020, when gold initially fell as investors raised cash. Historically, these selloffs tend to be brief before capital flows back into gold as a safe haven/liquidity hedge.

How we would play it

Our current thesis we implement in our institutional mandates: metal flows are currently reserved for oil and market neutral strategies - as long as the war continues. Once that changes - metals will become interesting again on the long side…and therefore in our portfolio.

In Other News…

Other hedge funds bleeded a lot of money recently - as data from Bloomberg shows.

As a ground rule, we like to stay away from war-induced volatility and shifted into cash - therefore we virtually didn't experience any drawdown.

I think the current situation highlights once again why it is important to have a systematic strategy that can be overruled by discretionary decisions in times like these.

We had long exposure to precious metals and long exposure to heating oil - we quickly decided to terminate both legs. Drawdown management is key, or as we say to our clients: we're happy to lose a few basis points in order to make percentage points.

Institutional Services

If you’re an institutional investor that wants to commit money into our strategy, receive a portfolio-overlay or copy our strategy to participate directly from our framework - contact us via info@lukas-kuemmerle.com

Till next Monday, Lukas

If you have any questions in the meantime, please feel free to contact me via X or Mail.