The Cocoa Saga Continues - Be Careful

The Cocoa Saga Continues - Be Careful

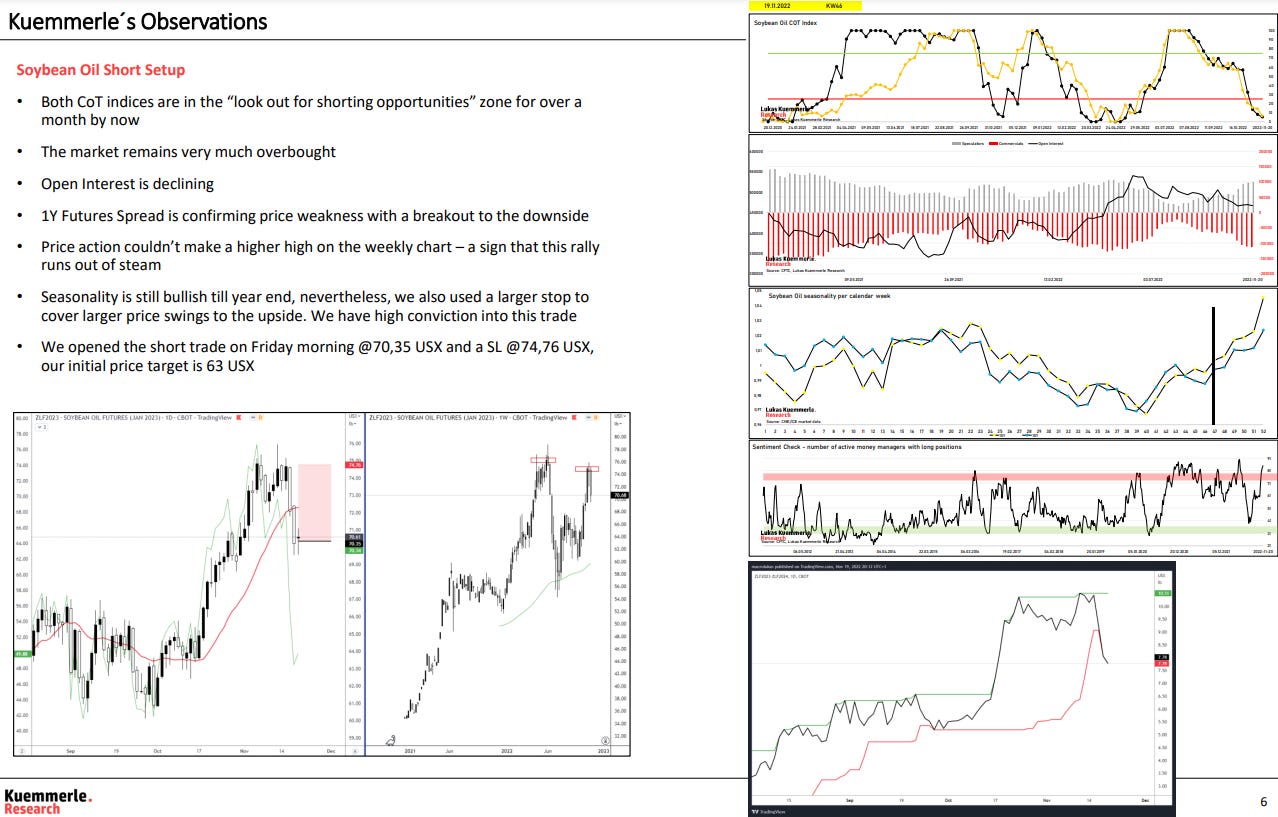

The Commodity Report #149

Top Commodity Trader is Long Cocoa

Pierre Andurand’s hedge fund bet on higher cocoa prices ahead of a massive surge last month, according to a Bloomberg article.

Andurand said his firm expects cocoa-beans production globally to be down at least 18% on an annual basis, compared to most analysts’ expectations of 10-11%. “This means that we will finish the year with the lowest stocks-to-grinding ratio ever, and potentially run out of inventories late in the year,” he added.

The firm sees that ratio — which measures stockpiles relative to annual demand — will end the 2023-24 season around 16% in a base-case scenario. That would push the indicator below the previous record low set in the mid-1970s, when prices hit $5,000 a ton — equivalent to about $26,000 when adjusted for inflation, according to Bloomberg calculations.

Still, the trade has become increasingly risky for cocoa traders as open interest wanes and margin calls rise. Total combined open interest for futures hasn’t been this low since 2021, exchange data show.

BEWARE THE RISKS

Meanwhile, farmers in the country will be paid 1,500 CFA francs a kilogram for the mid-crop, marking a 50% increase from the main-crop harvest. Prices are still well below the global market, but the raise could encourage more deliveries for processing and exporting.

Higher pay could also boost production in the longer-term by allowing farmers to reinvest in their crops. But markets remain focused on the near future, said John Goodwin, a senior commodity analyst at ArrowStream Inc in another interview with Bloomberg.

“The cocoa market is extremely short-sighted right now, so we probably won’t see a price reaction until the higher farm-level pricing bears fruit — literally and figuratively — in the form of higher shipments out, and it’s far from a guarantee that one will lead to the other,” Goodwin said.

Tailrisk Trade?

Hardly anybody is currently long treasuries, according to a client positioning survey of J.P Morgan clients. The survey tracks their clients’ positioning in Treasuries, asking them whether they are long, neutral or short. The net of the positions is close to flat, but outright shorts are unusually low, with the number of clients saying they are positioned that way near the nadir for the 20-year history of the survey, Bloomberg writes.

A reason for re-accelerating bond yields could be for example a commodity price-induced jump in the inflation data. This chart by Generali AM highlights this fact.

In Other News…

This week look out for the following:

CPI data on Wednesday

PPI data on Thursday

Prelim UoM Consumer Sentiment as well as USDA’s WASDE Report on Friday

A subscription costs $29 a month, and you will receive an additional in-depth report every Sunday evening at 6:00 PM CEST. Moreover - you will receive a quarterly economic growth report as well. That information will only be published to members and not the general public.

Till next Monday, Lukas

If you have any questions in the meantime, please feel free to contact me via Twitter or Mail.

The parabola will break eventually, probably via demand falling short.