31.05.21 - The Commodity Report

Chinas announcement to strengthen commodity price controls only had a minor impact on the market. Here are the latest developments.

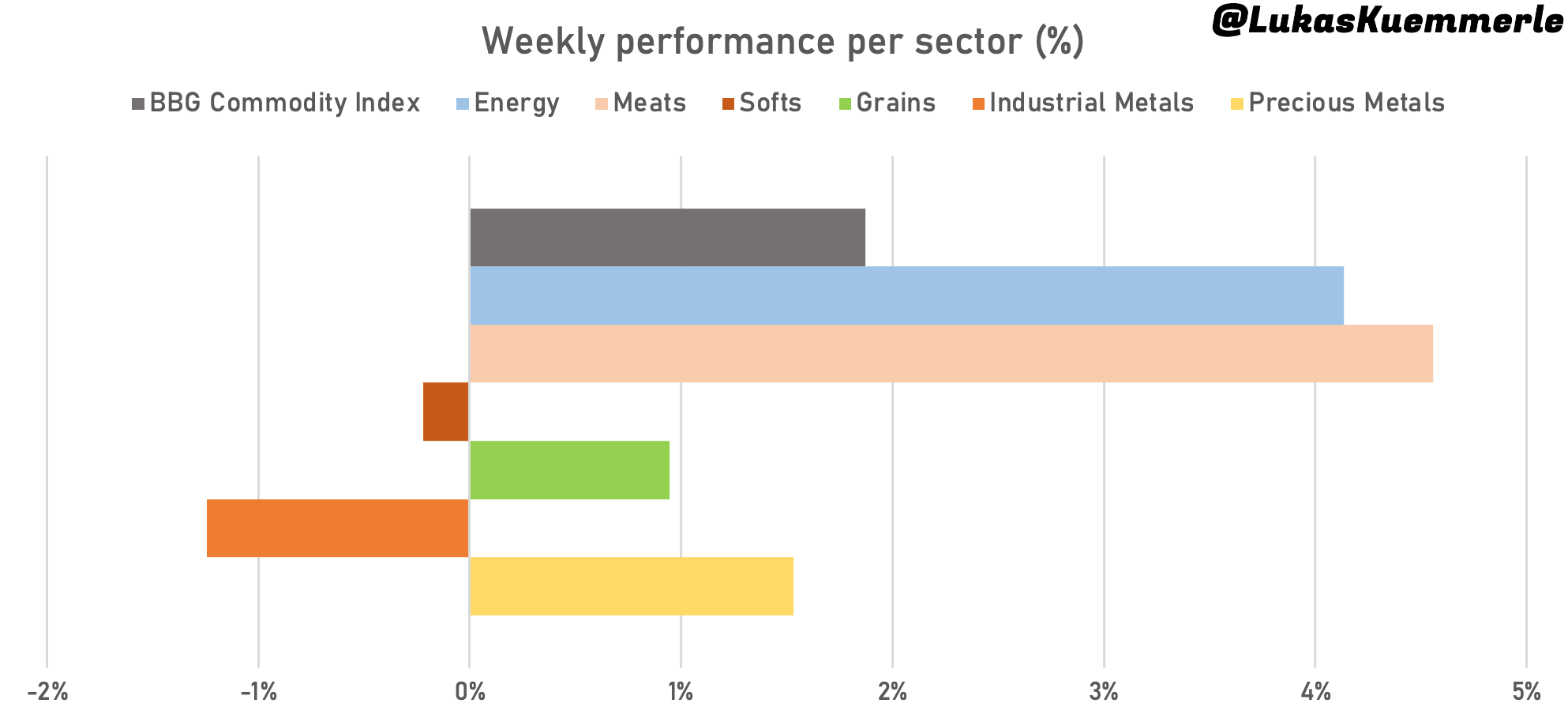

Top/Worst Performer Of The Week

In the last week of trading, we saw more gratifying results for commodities across the board. Among the winners were Energy and Meats but also Grains and Precious Metals. On the losing side we saw Industrial Metals. However this negative performance was only due to the enormous price drop at Iron Ore. On a broad front, it …